How to Build an Emergency Fund Faster

An emergency fund is one of the most important financial tools for achieving stability and long-term financial success. Unexpected expenses can occur at any time, whether due to medical emergencies, vehicle repairs, home maintenance, job loss, economic downturns, or family obligations. Without a dedicated emergency savings account, many people rely on credit cards, personal loans, or other forms of debt that can create long-term financial challenges.

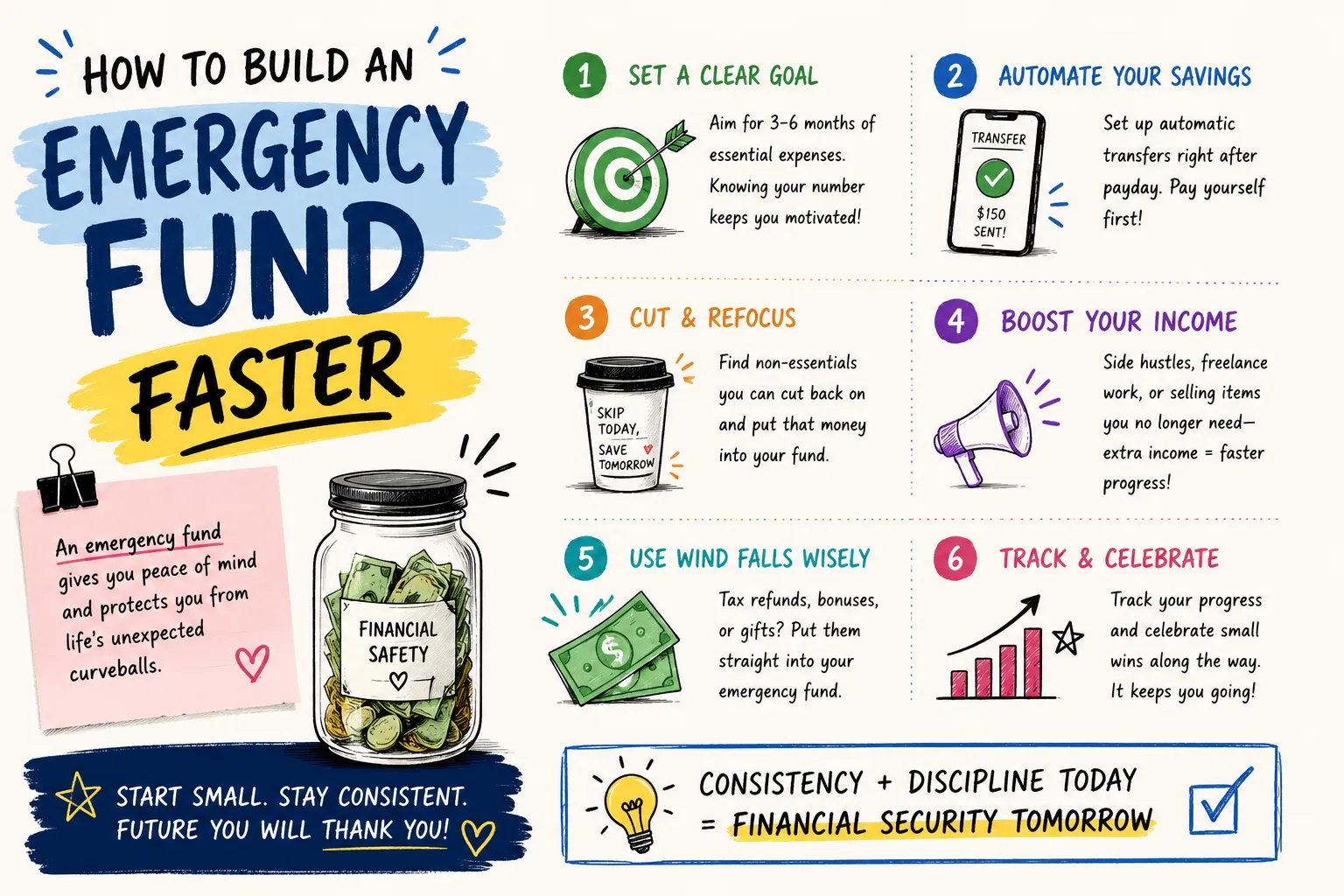

Building an emergency fund quickly provides peace of mind and helps protect your financial future. While saving several months of living expenses may seem overwhelming, strategic planning and disciplined money management can dramatically accelerate your progress. By implementing proven saving techniques, optimizing cash flow, reducing unnecessary expenses, and leveraging modern financial tools, you can create a substantial financial safety net faster than you might think.

This comprehensive guide explains practical methods to grow your emergency fund efficiently while maintaining your current lifestyle and long-term financial goals.

Why an Emergency Fund Matters

An emergency fund serves as a financial buffer between you and life's unexpected events. It allows you to handle emergencies without disrupting your financial plan or accumulating expensive debt.

Common situations where emergency savings become essential include:

- Job loss or income interruption

- Medical emergencies and healthcare expenses

- Vehicle repairs and maintenance

- Major home repairs

- Unexpected travel requirements

- Family emergencies

- Economic uncertainty and recessions

Financial experts typically recommend maintaining three to six months of essential living expenses in an easily accessible account. However, individuals with variable income, business owners, or freelancers may benefit from larger emergency reserves.

Determine Your Emergency Fund Target

The first step toward building emergency savings faster is establishing a clear target amount. Knowing your goal provides motivation and allows you to track progress effectively.

Calculate your monthly essential expenses, including:

- Housing costs

- Utilities

- Food and groceries

- Transportation

- Insurance premiums

- Healthcare expenses

- Minimum debt payments

| Monthly Expense Category | Estimated Amount |

|---|---|

| Housing | $2,000 |

| Utilities | $300 |

| Food | $700 |

| Transportation | $500 |

| Insurance | $400 |

| Healthcare | $300 |

| Total Monthly Expenses | $4,200 |

Using this example, a three-month emergency fund would require approximately $12,600, while a six-month reserve would equal $25,200.

Open a Dedicated High-Yield Savings Account

One of the fastest ways to accelerate emergency fund growth is to keep savings separate from daily spending accounts.

A dedicated high-yield savings account offers several advantages:

- Higher interest earnings

- Reduced temptation to spend savings

- Automatic savings tracking

- Improved cash management

- Easy access during emergencies

Modern online banks often provide significantly higher annual percentage yields compared to traditional checking accounts, allowing your emergency fund to grow more efficiently.

Automate Your Savings

Automation removes the need for constant decision-making and helps ensure consistent contributions.

Effective automation strategies include:

- Automatic transfers on payday

- Direct deposit splitting

- Recurring savings schedules

- Round-up savings programs

- Automatic investment-to-savings transfers

Treating savings as a mandatory expense increases consistency and reduces the likelihood of missed contributions.

Create a Zero-Based Budget

Zero-based budgeting assigns every dollar a specific purpose before the month begins. This method helps identify unnecessary spending and directs more money toward emergency savings.

Every dollar should be allocated to:

- Living expenses

- Debt repayment

- Investments

- Savings goals

- Emergency fund contributions

This budgeting approach creates accountability and maximizes savings potential.

Reduce Discretionary Spending

Temporary reductions in non-essential spending can significantly accelerate emergency fund growth.

Potential savings opportunities include:

- Dining out less frequently

- Reducing entertainment expenses

- Canceling unused subscriptions

- Limiting impulse purchases

- Reducing luxury spending

| Expense Category | Potential Monthly Savings |

|---|---|

| Dining Out | $300 |

| Streaming Services | $50 |

| Impulse Purchases | $200 |

| Entertainment | $150 |

| Total Savings | $700 |

Redirecting even modest amounts toward emergency savings can substantially shorten the time needed to reach your target.

Use Windfalls Strategically

Unexpected income presents an excellent opportunity to accelerate savings progress.

Consider allocating part or all of the following toward your emergency fund:

- Tax refunds

- Work bonuses

- Performance incentives

- Cash gifts

- Inheritance proceeds

- Side hustle earnings

- Investment gains

Many people achieve emergency savings goals months earlier by directing windfalls into dedicated reserve accounts.

Increase Your Income

Growing income often has a larger impact on savings rates than reducing expenses alone.

Popular income-boosting opportunities include:

- Freelancing

- Consulting

- Online businesses

- Affiliate marketing

- Content creation

- Part-time employment

- Professional certifications

- Passive income investments

Additional income streams provide both savings opportunities and greater financial resilience.

Sell Unused Assets

Many households possess valuable items that no longer serve a purpose.

Common examples include:

- Unused electronics

- Furniture

- Sporting equipment

- Collectibles

- Designer clothing

- Unused vehicles

Selling unused assets creates immediate cash that can strengthen your emergency reserve.

Optimize Debt Repayment Strategies

High-interest debt can significantly reduce available cash flow.

By reducing debt obligations, you create more room in your budget for emergency savings.

Effective debt management techniques include:

- Debt avalanche method

- Debt snowball method

- Refinancing high-interest loans

- Balance transfer opportunities

- Debt consolidation solutions

Lower interest expenses increase available resources for savings goals.

Build a Starter Emergency Fund First

Attempting to save six months of expenses immediately may feel overwhelming.

Instead, focus on smaller milestones:

- First $500

- First $1,000

- One month of expenses

- Three months of expenses

- Six months of expenses

Achieving smaller goals creates momentum and reinforces positive financial habits.

Leverage Cash Back and Rewards Programs

Many consumers overlook the value of cashback programs and rewards incentives.

Examples include:

- Credit card cashback rewards

- Shopping portals

- Retail loyalty programs

- Bank account bonuses

- Referral incentives

Redirecting rewards earnings into emergency savings can provide incremental growth over time.

Reduce Monthly Bills

Lower recurring expenses create permanent improvements in cash flow.

Consider negotiating:

- Insurance premiums

- Internet services

- Mobile phone plans

- Utility contracts

- Subscription services

Even modest monthly savings compound significantly over time.

| Bill Category | Monthly Savings Potential |

|---|---|

| Internet | $20-$50 |

| Insurance | $30-$100 |

| Phone Plan | $15-$50 |

| Streaming Services | $10-$40 |

Track Progress Consistently

Monitoring progress helps maintain motivation and accountability.

Track key metrics such as:

- Total emergency fund balance

- Monthly contributions

- Percentage of goal completed

- Interest earned

- Time remaining to target

Visual progress tracking often encourages continued commitment.

Avoid Common Emergency Fund Mistakes

Several common mistakes can slow savings progress.

- Keeping savings in checking accounts

- Using emergency funds for non-emergencies

- Failing to automate contributions

- Setting unrealistic goals

- Neglecting inflation adjustments

- Overinvesting emergency reserves in volatile assets

An emergency fund should prioritize accessibility, stability, and liquidity.

Emergency Funds During Economic Uncertainty

Periods of inflation, recession risk, and market volatility make emergency savings even more important.

Financial resilience often depends on having adequate cash reserves available when unexpected events occur.

Benefits include:

- Reduced reliance on debt

- Greater financial flexibility

- Improved investment decision-making

- Lower financial stress

- Enhanced long-term wealth preservation

Balancing Emergency Savings and Investing

Many people wonder whether to prioritize investing or emergency savings.

In most cases, building a foundational emergency fund should come before aggressive investing.

A balanced approach may involve:

- Building a starter emergency fund first

- Capturing employer retirement matches

- Eliminating high-interest debt

- Completing emergency fund goals

- Increasing long-term investments

This strategy provides both protection and wealth-building opportunities.

Long-Term Benefits of Emergency Savings

Beyond financial protection, emergency funds contribute to long-term success by improving decision-making and reducing stress.

Individuals with adequate emergency savings often experience:

- Greater confidence during uncertainty

- Improved investment discipline

- Reduced financial anxiety

- Better career flexibility

- Enhanced financial independence

The financial security provided by an emergency fund extends far beyond the account balance itself.

Conclusion

Building an emergency fund faster requires a combination of strategic planning, disciplined spending, income optimization, and consistent saving habits. By establishing clear savings targets, automating contributions, reducing unnecessary expenses, increasing income opportunities, and leveraging high-yield savings accounts, you can accelerate your progress significantly.

An emergency fund is more than a savings account—it is a critical financial foundation that protects your wealth, supports long-term goals, and provides peace of mind during uncertain times. The sooner you begin building your emergency reserve, the stronger your overall financial position becomes.