How Inflation Impacts Personal Finances

Inflation is one of the most powerful yet often misunderstood forces shaping personal finance, investment performance, and long-term wealth creation. It quietly reduces the purchasing power of money over time, meaning that the same amount of income buys fewer goods and services in the future than it does today. While inflation is a normal part of most modern economies, its effects can significantly influence savings, investments, debt, and overall financial stability.

For individuals and families, understanding inflation is essential for making informed financial decisions. Whether you are budgeting monthly expenses, investing in the stock market, planning for retirement, or managing debt, inflation plays a direct role in determining your real financial outcomes. Ignoring inflation can lead to underestimating future costs, insufficient retirement savings, and reduced long-term wealth.

This detailed guide explores how inflation impacts different areas of personal finance and provides practical strategies to protect and grow your wealth in inflationary environments.

What Is Inflation?

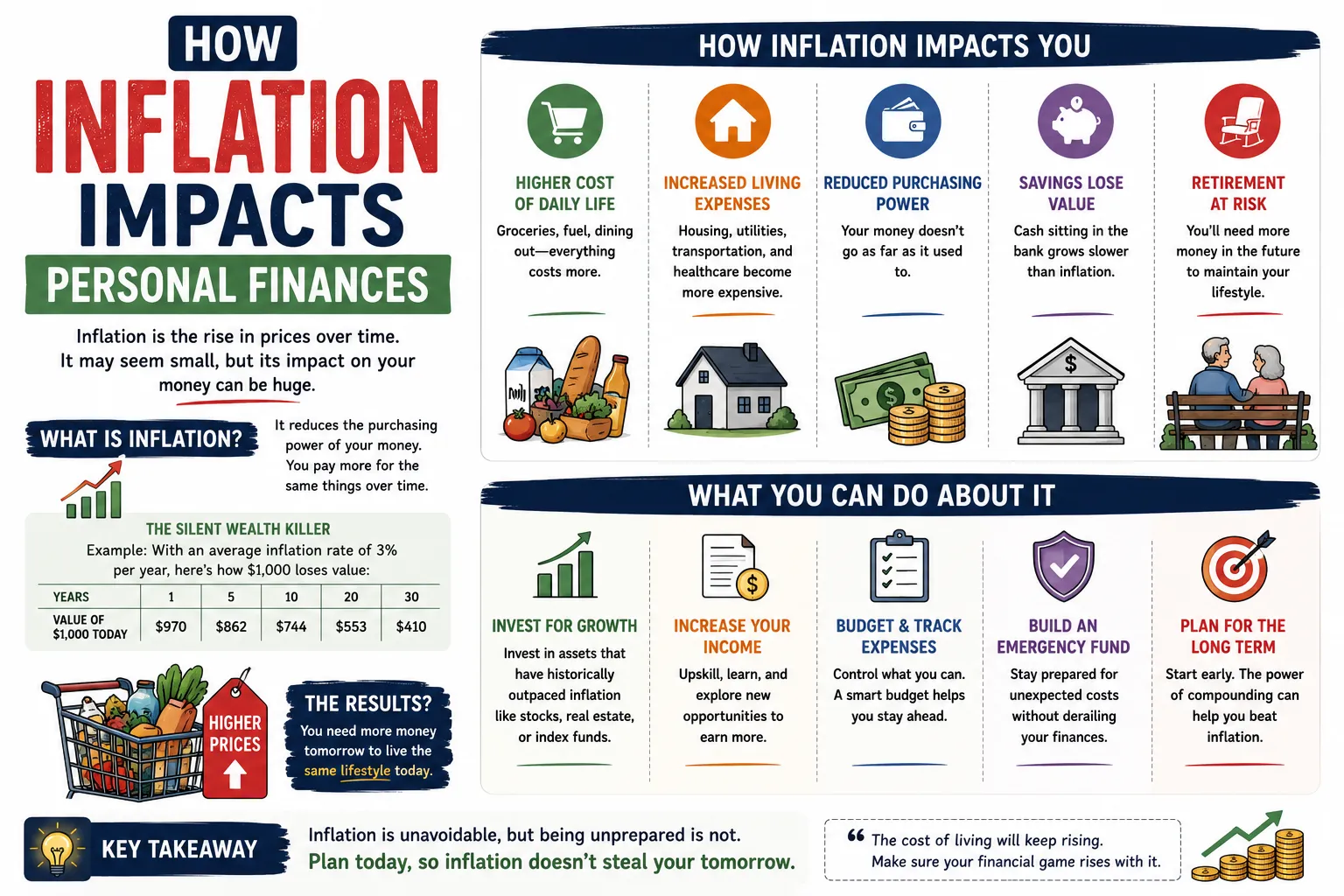

Inflation refers to the general increase in prices of goods and services over time. As prices rise, each unit of currency loses value in terms of purchasing power.

In simple terms:

- When inflation rises, your money buys less

- When inflation is stable, purchasing power is preserved

- When inflation is high, financial planning becomes more challenging

Inflation is typically measured using indices such as consumer price indexes that track changes in the cost of everyday goods like food, housing, transportation, healthcare, and education.

How Inflation Affects Purchasing Power

The most direct impact of inflation is the decline in purchasing power. Even modest inflation rates can significantly reduce the value of money over time.

| Years | Value of $100 (at 3% inflation) |

|---|---|

| 0 Years | $100 |

| 10 Years | $74 |

| 20 Years | $55 |

| 30 Years | $41 |

This gradual erosion of value makes long-term financial planning essential.

Impact of Inflation on Savings

One of the most significant effects of inflation is its impact on savings accounts and cash holdings. While keeping money in savings provides safety and liquidity, inflation reduces its real value over time if returns do not keep pace.

For example, if your savings account earns a lower interest rate than inflation, your real wealth is effectively decreasing even though your balance appears stable.

Key challenges include:

- Low interest returns on traditional savings accounts

- Reduced real purchasing power

- Delayed financial goals due to stagnant growth

This is why many financial experts recommend balancing savings with investment strategies that can outpace inflation.

Inflation and Income Growth

Income plays a critical role in maintaining financial stability during inflationary periods. If wages do not increase at the same rate as inflation, individuals experience a decline in real income.

This means that even if your salary remains the same or increases slightly, your ability to afford goods and services may still decline.

Common impacts include:

- Reduced disposable income

- Increased pressure on monthly budgets

- Delayed savings goals

- Greater reliance on credit

To counter this, many professionals focus on skill development, career advancement, and income diversification.

Inflation and Cost of Living

One of the most visible effects of inflation is the rising cost of living. Essential expenses such as housing, groceries, healthcare, and transportation often increase over time.

| Expense Category | Inflation Impact |

|---|---|

| Housing | Rising rent and property prices |

| Food | Increasing grocery and dining costs |

| Healthcare | Higher medical service expenses |

| Education | Rising tuition fees |

| Transportation | Fuel and vehicle cost increases |

As expenses increase, individuals must adjust budgets or risk financial strain.

Impact on Investments

Inflation has a complex relationship with investments. While it can reduce the value of cash holdings, certain assets may benefit from inflationary environments.

Investment considerations include:

- Stock markets may provide inflation-adjusted growth over time

- Real estate often acts as a hedge against inflation

- Fixed-income investments may lose value in high inflation periods

- Commodities may rise during inflationary cycles

Understanding asset behavior during inflation is essential for building a resilient portfolio.

Real Returns vs Nominal Returns

It is important to distinguish between nominal returns and real returns.

| Type | Description |

|---|---|

| Nominal Return | Return before inflation adjustment |

| Real Return | Return after inflation adjustment |

For example, if your investment returns 8% annually but inflation is 4%, your real return is only 4%.

Inflation and Debt Management

Inflation affects debt in both positive and negative ways. Fixed-rate debt becomes easier to repay over time because the real value of money decreases.

Benefits of inflation for borrowers include:

- Reduced real value of fixed loan payments

- Potential wage growth improving repayment ability

- Predictable debt obligations

However, variable interest rate debt can become more expensive if interest rates rise with inflation.

Impact on Retirement Planning

Inflation is one of the most critical factors in retirement planning. Since retirement may last 20 to 30 years or more, even small inflation rates can significantly increase future living costs.

Without proper planning, retirees may face:

- Insufficient retirement savings

- Reduced purchasing power in retirement

- Increased financial stress during later life stages

This is why retirement projections often include inflation-adjusted growth assumptions.

Inflation Protection Strategies

Protecting personal finances from inflation requires a combination of income growth, investment diversification, and strategic financial planning.

Effective strategies include:

- Investing in diversified stock portfolios

- Real estate investment for long-term appreciation

- Inflation-protected securities

- Increasing income through skill development

- Reducing unnecessary expenses

- Maintaining emergency funds

Budgeting During Inflation

Inflation requires adjustments to personal budgets to maintain financial stability.

Key budgeting strategies include:

- Tracking monthly expenses closely

- Reducing discretionary spending

- Prioritizing essential expenses

- Increasing savings rate when possible

- Reviewing subscriptions and recurring costs

Regular budget updates help maintain control during rising price environments.

Inflation and Financial Independence

Inflation plays a major role in determining the timeline for financial independence. Since living expenses increase over time, financial independence calculations must account for inflation-adjusted costs.

Individuals pursuing financial independence often focus on:

- Generating inflation-resistant income streams

- Building diversified investment portfolios

- Increasing passive income sources

- Maintaining high savings rates

Common Mistakes During Inflationary Periods

| Mistake | Financial Impact |

|---|---|

| Holding Excess Cash | Loss of purchasing power |

| No Investment Strategy | Weak long-term growth |

| Ignoring Rising Costs | Budget imbalance |

| Fixed Income Overreliance | Lower real returns |

| No Income Growth Plan | Reduced financial stability |

Building an Inflation-Resilient Financial Plan

A strong financial plan should consider inflation as a long-term factor affecting every financial decision.

Key components include:

- Income growth strategy

- Diversified investment portfolio

- Emergency fund planning

- Debt management strategy

- Retirement planning with inflation adjustments

- Expense optimization system

These elements work together to protect wealth and ensure long-term financial stability.

Final Thoughts

Inflation is an unavoidable economic force that influences nearly every aspect of personal finance. From savings and investments to debt, income, and retirement planning, its impact is both widespread and long-lasting. While inflation can erode purchasing power, it also creates opportunities for individuals who understand how to adapt their financial strategies.

By focusing on income growth, strategic investing, diversified assets, and disciplined budgeting, individuals can reduce the negative effects of inflation and build stronger financial futures. Understanding inflation is not just about protecting money—it is about making smarter decisions that preserve and grow wealth over time.