Financial Planning Tips for Young Professionals

Financial planning is one of the most important life skills young professionals can develop early in their careers. The financial decisions made during your twenties and thirties often have a greater long-term impact than decisions made later in life because of the power of compound growth, career advancement, and wealth accumulation over time.

Many young professionals begin earning a steady income for the first time and experience increased financial freedom. While higher income creates opportunities, it also introduces new responsibilities including budgeting, debt management, retirement planning, insurance decisions, tax planning, investing, and wealth preservation.

The earlier financial planning begins, the easier it becomes to build long-term financial security, achieve major life goals, and create financial independence. Whether your objective is purchasing a home, building an investment portfolio, retiring early, starting a business, or simply reducing financial stress, establishing strong financial habits today can create significant benefits for decades.

This comprehensive guide explores practical financial planning tips designed specifically for young professionals who want to maximize income, grow wealth, and build a strong financial foundation.

Why Financial Planning Matters Early in Life

Many individuals delay financial planning because retirement and wealth-building goals seem distant. However, time is one of the most valuable assets available to investors and savers.

Starting early provides advantages such as:

- Greater compound investment growth

- Higher retirement account balances

- Improved financial flexibility

- Reduced debt burden

- Stronger emergency preparedness

- Increased wealth accumulation opportunities

- Lower financial stress

Financial planning is not about restricting your lifestyle. It is about creating a system that aligns spending, saving, and investing with your long-term goals.

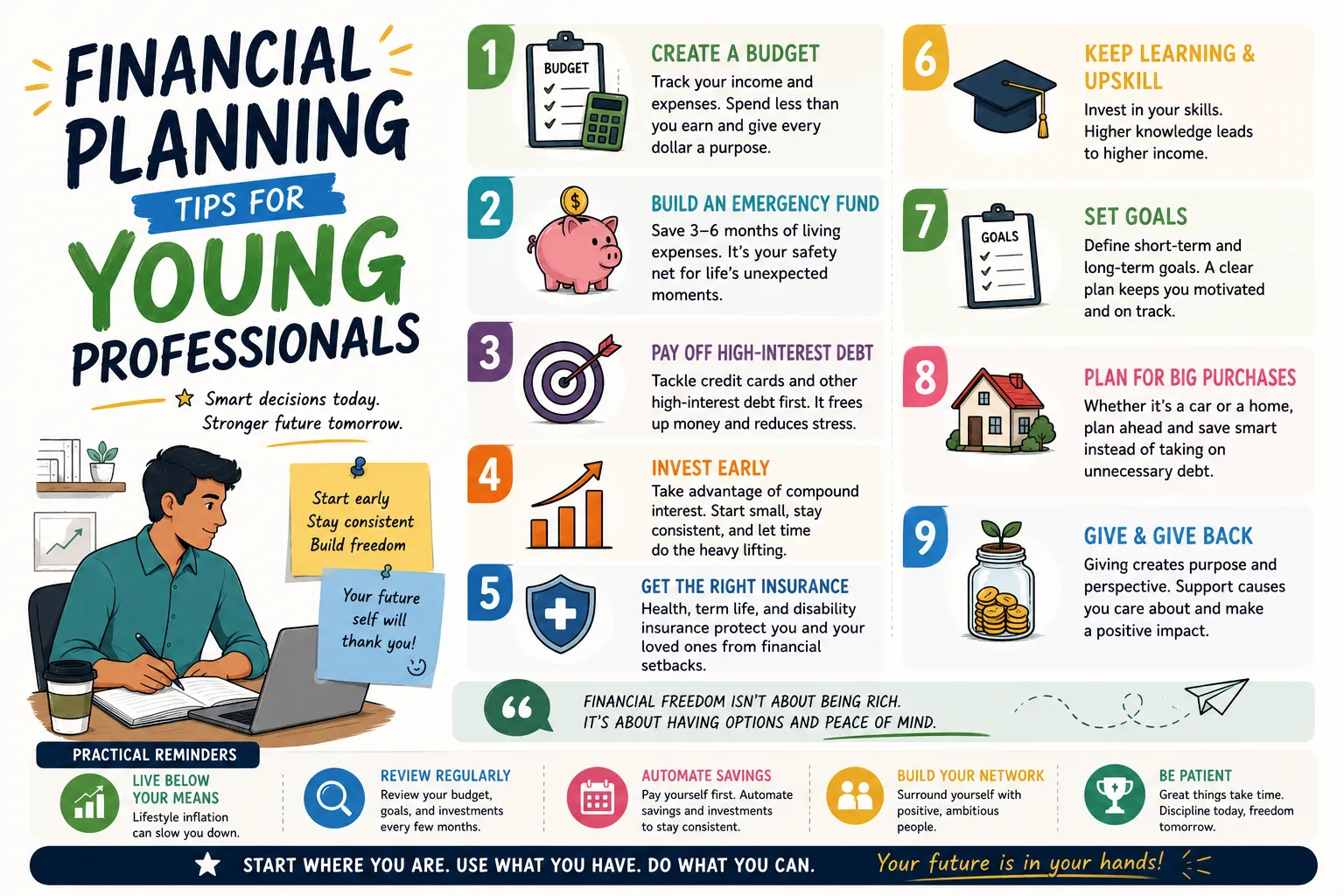

Create Clear Financial Goals

Successful financial planning begins with clearly defined objectives. Without specific goals, it becomes difficult to prioritize spending and measure progress.

Common goals for young professionals include:

- Building an emergency fund

- Paying off student loans

- Purchasing a home

- Starting a business

- Investing for retirement

- Creating passive income streams

- Achieving financial independence

| Goal Type | Time Horizon | Examples |

|---|---|---|

| Short-Term | 1-3 Years | Emergency fund, travel savings |

| Medium-Term | 3-10 Years | Home purchase, business startup |

| Long-Term | 10+ Years | Retirement, financial independence |

Develop a Budget That Works

A budget provides visibility into income and expenses. Rather than restricting spending, budgeting helps ensure money is allocated intentionally.

A commonly used framework is the 50/30/20 model.

| Allocation | Purpose |

|---|---|

| 50% | Needs and essentials |

| 30% | Lifestyle and discretionary spending |

| 20% | Savings and investments |

As income grows, increasing the percentage allocated to investments can significantly accelerate wealth creation.

Build an Emergency Fund First

An emergency fund serves as a financial safety net and protects against unexpected expenses such as medical emergencies, job loss, vehicle repairs, or economic downturns.

Financial experts often recommend maintaining:

- 3 months of expenses at minimum

- 6 months for greater security

- 12 months for maximum flexibility

Keeping emergency savings in a liquid, easily accessible account ensures funds remain available when needed.

Understand the Power of Compound Interest

Compound growth allows investments to generate returns on both original contributions and previous earnings.

| Monthly Investment | Years | Estimated Value at 8% |

|---|---|---|

| $250 | 30 | $372,000+ |

| $500 | 30 | $745,000+ |

| $1,000 | 30 | $1.49 Million+ |

The earlier investments begin, the more powerful compounding becomes.

Prioritize Retirement Planning

Retirement planning should begin with your first paycheck.

Benefits of early retirement investing include:

- Longer growth periods

- Potential employer matching contributions

- Tax advantages

- Reduced future contribution requirements

Young professionals who begin saving early often require significantly less effort to reach retirement goals compared to those who delay.

Invest Consistently

Successful investors focus on consistency rather than attempting to predict short-term market movements.

Strategies include:

- Automatic investment contributions

- Dollar-cost averaging

- Diversified portfolios

- Long-term investment horizons

Consistent investing removes emotion from financial decisions and encourages disciplined wealth building.

Manage Debt Strategically

Debt management plays a critical role in financial planning.

Not all debt is equally harmful.

| Debt Type | Priority Level |

|---|---|

| Credit Card Debt | Very High |

| Personal Loans | High |

| Auto Loans | Moderate |

| Student Loans | Moderate |

| Mortgage | Lower |

Eliminating high-interest debt often provides guaranteed financial returns by reducing interest expenses.

Avoid Lifestyle Inflation

One of the biggest challenges facing young professionals is lifestyle inflation. As income increases, spending often rises proportionally.

Instead of spending every raise, consider allocating a significant portion toward:

- Investments

- Retirement accounts

- Debt reduction

- Emergency savings

- Passive income assets

This strategy accelerates wealth accumulation while maintaining financial flexibility.

Protect Your Income with Insurance

Income is often a young professional's most valuable asset.

Important insurance considerations include:

- Health insurance

- Disability insurance

- Life insurance (if dependents exist)

- Renters insurance

- Professional liability coverage where applicable

Proper protection reduces financial risk and safeguards long-term plans.

Improve Financial Literacy

Financial education is one of the highest-return investments available.

Key topics to study include:

- Investing fundamentals

- Tax planning

- Retirement accounts

- Real estate investing

- Risk management

- Personal budgeting

- Wealth preservation

Knowledge helps individuals make informed financial decisions and avoid costly mistakes.

Create Multiple Income Streams

Relying entirely on one paycheck can create financial vulnerability.

Additional income opportunities include:

- Freelancing

- Consulting

- Dividend investing

- Rental income

- Online businesses

- Digital products

- Affiliate marketing

- Content creation

Multiple income streams can improve cash flow and accelerate financial goals.

Optimize Tax Planning

Young professionals often overlook tax-saving opportunities.

Tax-efficient strategies may include:

- Retirement account contributions

- Health savings accounts

- Tax-efficient investing

- Education credits

- Employer benefit programs

Keeping more of your earnings can significantly improve long-term wealth accumulation.

Build a Strong Credit Profile

A healthy credit profile can impact:

- Mortgage approval

- Auto financing rates

- Credit card benefits

- Insurance premiums

- Rental applications

Best practices include paying bills on time, maintaining low credit utilization, and monitoring credit reports regularly.

Track Net Worth Annually

Net worth provides a comprehensive picture of financial progress.

| Assets | Liabilities |

|---|---|

| Investments | Loans |

| Cash Savings | Credit Card Debt |

| Retirement Accounts | Mortgage Balances |

| Real Estate | Personal Debt |

Monitoring net worth helps measure progress toward long-term financial independence.

Financial Habits That Create Long-Term Wealth

Many financially successful individuals share similar habits:

- Living below their means

- Investing consistently

- Tracking expenses

- Avoiding excessive debt

- Maintaining emergency reserves

- Seeking financial education

- Thinking long term

Small habits repeated consistently often create extraordinary financial results over time.

Common Financial Mistakes Young Professionals Make

| Mistake | Potential Impact |

|---|---|

| Delaying Investing | Lost compound growth |

| Overspending | Reduced savings capacity |

| No Emergency Fund | Financial instability |

| High-Interest Debt | Wealth destruction |

| Ignoring Retirement Planning | Future funding gaps |

| Lack of Budgeting | Poor cash flow control |

Creating a Financial Independence Roadmap

Financial independence does not happen overnight. It is built through intentional actions over many years.

- Establish financial goals.

- Create a budget.

- Build emergency savings.

- Eliminate expensive debt.

- Maximize retirement contributions.

- Invest consistently.

- Create multiple income streams.

- Optimize taxes.

- Track net worth.

- Continue improving financial knowledge.

This roadmap creates a structured path toward long-term financial freedom.

Final Thoughts

Financial planning is one of the most valuable investments young professionals can make. The decisions made early in life often determine future financial flexibility, retirement readiness, and wealth-building potential. By establishing clear goals, budgeting effectively, building emergency reserves, managing debt responsibly, investing consistently, and continuously improving financial literacy, young professionals can create a strong foundation for long-term success.

The most important step is simply getting started. Small actions taken today can compound into substantial financial advantages tomorrow. With discipline, consistency, and a long-term perspective, financial independence becomes an achievable goal rather than a distant dream.